"Stop Mixing Business and Personal Travel Expenses! Discover How Navan Can Save You Time and Money"

Managing business and personal travel expenses can be a complex and often confusing task, especially when both types of expenses occur simultaneously. Not to mention how fast a trip can go by, what receipts weren’t collected, which were, which part was business, and which part was personal.

This article will explore the importance of differentiating and tracking these expenses in an automated way, discuss effective methods for doing so, and highlight how tools like Navan and Refresh.me simplify the process. By the end of this article, you'll have a clear understanding of how to manage your travel expenses efficiently, ensuring compliance with tax regulations and maximizing your travel benefits.

Importance of Tracking Business vs. Personal Expenses

Keeping business and personal expenses separate is crucial for several reasons. Mixing these expenses can lead to accounting errors, making it difficult to accurately report business expenses on your taxes. This can result in lost deductions and potential issues with tax authorities. Additionally, separating expenses ensures better financial management and clarity in understanding your business's profitability.

Real-World Scenario

Imagine you're a small business owner attending a conference in New York. You decide to extend your stay for a personal vacation. Without a clear system in place, it becomes challenging to differentiate the costs associated with the conference (business expense) from your vacation (personal expense). This confusion can lead to incorrect bookkeeping, resulting in either over-reporting or under-reporting your business expenses. How about the tax deductions you could be missing out on?

Methods for Keeping Track of Expenses

Separate Bank Accounts and Credit Cards: Use dedicated accounts and cards for business transactions. This helps in easily identifying and tracking expenses without the need to sift through mixed transactions.

Detailed Expense Reports: Maintain detailed records of your expenses. Include receipts, dates, descriptions, and the purpose of each expense. This practice helps in accurately categorizing expenses and supports your claims during tax filing.

Digital Tools and Apps: Utilize expense tracking software like Navan and Refresh.me. These tools automate the tracking process, ensuring accuracy and saving time.

How Navan Simplifies Expense Tracking

Navan offers a comprehensive solution for managing travel expenses. Here’s how:

Automatic Categorization: Navan automatically categorizes expenses as business or personal based on predefined rules. This feature reduces manual effort and minimizes errors.

Integration: By automating the reconciliation process and integrating directly with tools like Refresh.me and QuickBooks Online, finance teams can eliminate frustrating, manual work and close the books faster.

Real-Time Expense Tracking: With real-time tracking, you can monitor your expenses as they occur, ensuring immediate identification and correction of any discrepancies.

Integration with Accounting Software: Navan integrates seamlessly with popular accounting tools, ensuring that your expense data is always up-to-date and accurate.

How Refresh.me Enhances Expense Management

Refresh.me complements Navan by providing additional features for expense management:

Expense Insights and Analytics: Refresh.me offers detailed insights and analytics, helping you understand spending patterns and make informed decisions.

Customizable Reports: Generate customized reports that meet your specific needs, whether for tax filing or internal reviews.

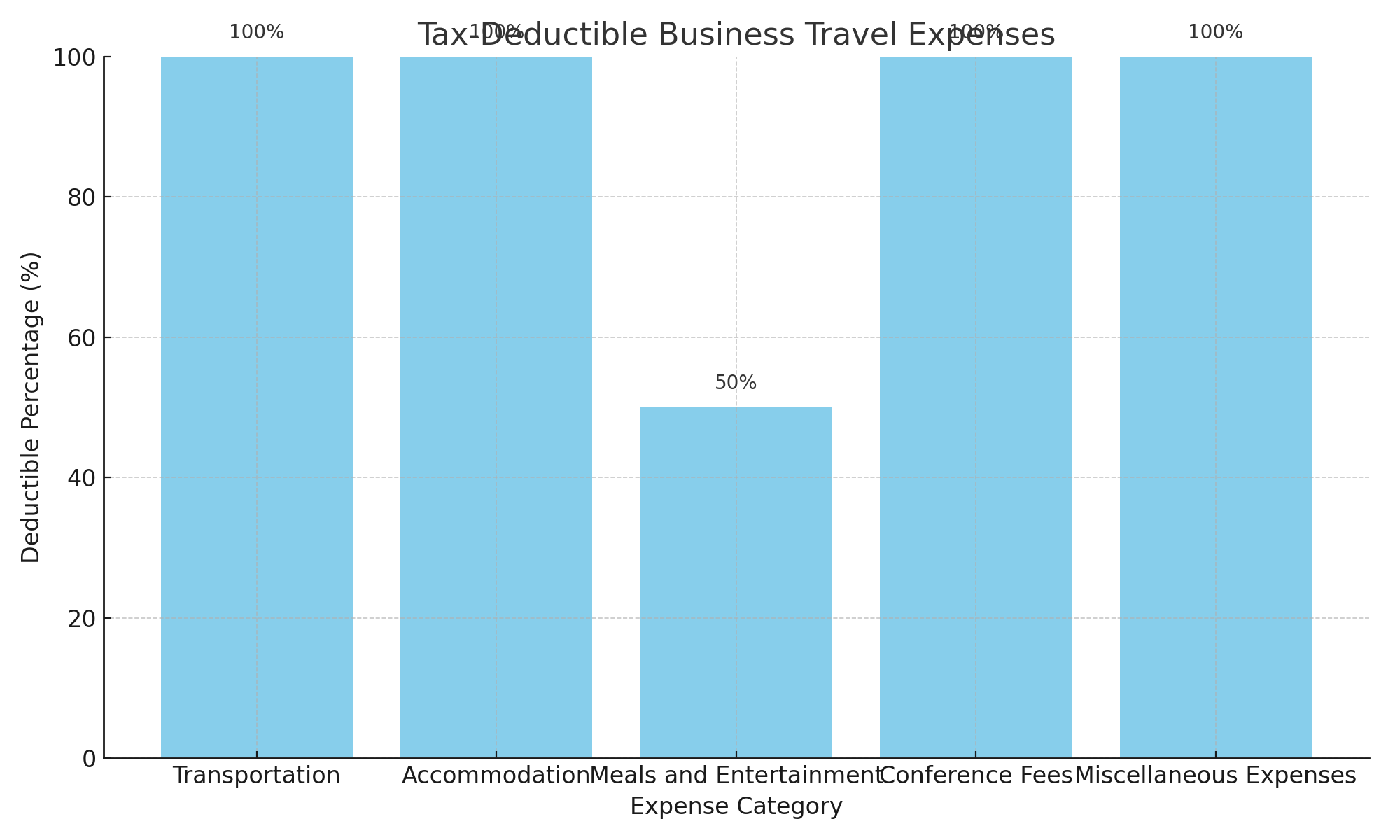

What Business Travel Expenses are Tax-Deductible

Understanding what qualifies as a tax-deductible business travel expense is crucial. Common deductible expenses include:

Transportation: Costs of flights, trains, taxis, and car rentals for business purposes.

Accommodation: Hotel stays and lodging expenses incurred during business trips.

Meals and Entertainment: Business-related meals and entertainment, typically up to 50% of the cost.

Conference Fees: Registration fees for business-related conferences and events.

Miscellaneous Expenses: Other necessary expenses such as internet fees, shipping of business materials, and tips.

Business Tax Deductible Expenses

Effectively managing business and personal travel expenses is essential for maintaining accurate financial records and maximizing tax benefits. By using tools like Navan and Refresh.me, you can simplify the tracking process, ensure compliance with tax regulations, and gain valuable insights into your spending patterns. Start integrating these solutions into your financial management practices today to experience the benefits firsthand.

For further reading on expense management and financial tools, check out our other articles and resources. Don't forget to subscribe to our newsletter for the latest tips and updates!

Master Your Money: How to Excel at Cashflow Management with Free Spreadsheets

If you're reading this, you're probably looking for some help managing your cashflow during these tricky financial times. Don't worry, you're not alone, and I've got your back! In this article, I'll walk you through how to manage your cash flow for free using spreadsheets and trust me, it's easier than you might think.

Understanding Cashflow:

First things first, let's talk about what cashflow means. Cashflow is the movement of money in and out of your bank account. When money comes in, that's called income. When money goes out, that's called expenses. Managing your cashflow is all about making sure you have enough money to cover your expenses without going broke. Plus, no matter what business structure you have, we all must pay taxes, essentially cashflow ensures the money is even there to do your primary legal priority.

To get a clearer grasp, let's break it down into two main components:

Income: Income refers to any money that comes into your possession. This could be from your job, side hustles, investments, or any other sources of revenue. It's the cash flow that fills your pocket.

Expenses: On the other hand, expenses encompass all the money flowing out of your account. This includes your bills, groceries, rent or mortgage payments, entertainment expenses, and anything else you spend money on.

Types of Cashflow:

Understanding cashflow also involves recognizing the different types:

Positive Cashflow: This is the ideal scenario where your income exceeds your expenses. Essentially, you're making more money than you're spending. Positive cashflow allows you to save, invest, and build a financial cushion for the future.

Negative Cashflow: Conversely, negative cashflow occurs when your expenses outweigh your income. This can lead to financial stress, debt accumulation, and difficulty covering essential expenses. It's like trying to fill a leaky bucket – no matter how much water you pour in, it keeps draining out.

Significance of Cashflow Management:

Managing your cashflow effectively is crucial for several reasons:

1. Financial Stability: By tracking your cashflow, you gain insight into your financial situation. This allows you to make informed decisions and avoid overspending.

2. Debt Management: Understanding your cashflow helps you identify areas where you can cut back on expenses, freeing up money to pay off debts faster.

3. Emergency Preparedness: A well-managed cashflow enables you to build an emergency fund, providing a safety net for unexpected expenses like medical bills or car repairs.

4. Goal Achievement: Whether it's buying a home, starting a business, or traveling the world, managing your cashflow puts you in control of your financial destiny, helping you reach your goals faster.

Tracking Cashflow Using Spreadsheets:

Now that you have grasped the concept of cashflow, let's talk about how spreadsheets come into play. Spreadsheets are like your financial command center – they allow you to organize and analyze your cashflow data with ease. By creating a simple spreadsheet, you can monitor your income and expenses, identify trends, and make informed financial decisions.

Remember, mastering cashflow management takes time and practice, but with dedication and the right tools, you can achieve financial peace of mind. So, embrace the journey, stay proactive, and watch your financial future flourish!

Why Spreadsheets?

Spreadsheets are like your personal financial assistant but without the cost! They offer a myriad of benefits that make them an invaluable resource for anyone looking to take control of their finances. First and foremost, spreadsheets are completely free. In times when every penny counts, saving money wherever possible is crucial. Unlike specialized financial management software that often comes with a hefty price tag, spreadsheets are accessible to everyone, regardless of budget constraints.

Moreover, spreadsheets are highly customizable, allowing you to tailor your financial management tool to fit your unique needs and preferences perfectly. Whether you have a simple income and expenses setup or need a more complex system to track multiple revenue streams and expenditure categories, spreadsheets can accommodate it all. This adaptability ensures that you can create a cashflow management tool that suits your specific financial situation.

Another significant advantage of spreadsheets is their ability to provide a clear and organized visualization of your financial data. With neatly arranged rows and columns, you can easily see your income, expenses, and overall cashflow at a glance. This visual representation makes it much easier to understand your financial situation and identify any areas that may need attention. Plus, you can customize the formatting to highlight important information or trends, making it even easier to spot potential issues or opportunities for improvement.

Additionally, spreadsheets offer unparalleled accessibility, allowing you to manage your finances anytime, anywhere. Whether you're at home on your computer or out and about with your smartphone, as long as you have access to your spreadsheet program and an internet connection, you can update your financial information in real time. This accessibility ensures that you always have a clear picture of your cashflow, even when you're on the go.

Despite their powerful capabilities, spreadsheets are surprisingly easy to use, especially once you become familiar with the basics. Most spreadsheet programs offer user-friendly interfaces and a wide range of pre-designed templates to help you get started quickly. Additionally, there are countless online tutorials and resources available to help you learn how to maximize the potential of your spreadsheet, making it accessible even for beginners. You can also take your completed spreadsheets and attach them to an AI tool to extract information needed to grow your business and understand how to better budget.

Getting Started:

1. Choose Your Spreadsheet Program: Before you start creating your cashflow spreadsheet, decide which spreadsheet program you want to use. As mentioned earlier, Google Sheets is a great option because it's free and accessible with just a Google account. If you prefer, you can also use Microsoft Excel, which offers similar features.

2. Open a New Spreadsheet: Once you've chosen your spreadsheet program, open a new spreadsheet. In Google Sheets, you can do this by navigating to Google Drive and clicking on the "+ New" button, then selecting "Google Sheets."

3. Label Your Columns: Now it's time to label your columns. Think about the information you'll need to track your cashflow effectively. Here are some suggested column labels:

Date: This column will contain the date of each transaction.

Description: Use this column to describe what the transaction was for (e.g., groceries, rent, paycheck).

Income: Here, you'll record any money that comes into your account, such as your salary, freelance income, or gifts.

Expenses: This column is for tracking any money that goes out of your account, including bills, groceries, entertainment expenses, etc.

Balance: In this column, you'll calculate your account balance after each transaction.

4. Format Your Spreadsheet: Take a moment to format your spreadsheet to make it easier to read and use. You can adjust the column widths, change the font size, and add borders to separate your data. This step isn't essential, but it can make your spreadsheet more visually appealing and user-friendly.

5. Set Up Your Formulas (Optional- not required): Next, you'll want to set up formulas to calculate your account balance automatically. In the first row of the "Balance" column, enter your starting balance. Then, in the cells below, use a simple formula to calculate the balance after each transaction. For example, if cell A2 contains your starting balance and cell C2 contains your first income transaction, you can use the formula `=A2+C2-D2` in cell E2 to calculate the new balance.

6. Start Recording Transactions: With your spreadsheet set up, it's time to start recording your transactions. Every time you receive income or spend money, enter the details into your spreadsheet. Be sure to fill in each column accurately and consistently. This will ensure that your cashflow tracker is as useful and reliable as possible.

By following these steps, you'll be well on your way to creating a comprehensive cashflow spreadsheet that will help you manage your finances effectively. Remember, the key is to stay organized and diligent about recording your transactions regularly. With practice, you'll become more comfortable using spreadsheets to track your cashflow, and you'll gain valuable insights into your financial habits and patterns.

Analyzing Your Cashflow:

Once you've diligently tracked your cashflow for a significant period, it's crucial to step back and take a comprehensive look at your financial data. Think of your cashflow spreadsheet as a treasure trove of insights waiting to be discovered. Now, it's time to unearth these insights and use them to make informed decisions for your business.

Start by examining your income and expenses over the past few months. Look for patterns and trends. Are there certain times of the year when your income tends to spike? Are there any months where you consistently overspend? Understanding these patterns will help you anticipate fluctuations in your cashflow and plan accordingly.

Next, take a closer look at your expenses. Are there any recurring expenses that you could reduce or eliminate? Are there areas where you're overspending? Perhaps you're paying for services or subscriptions that you no longer need. By identifying these areas of opportunity, you can free up valuable resources to invest back into your business.

It's also important to analyze your profit margins. Look at the ratio between your income and expenses. Are you operating at a healthy profit margin, or are your expenses eating into your profits? If you're struggling to maintain a positive cashflow, it may be time to reevaluate your pricing strategy or find ways to reduce your costs.

Furthermore, consider your accounts receivable and accounts payable. Are you waiting too long to collect payments from your customers? Are you paying your suppliers on time? Delayed payments can have a significant impact on your cashflow, so it's essential to stay on top of your invoicing and payment schedules.

Finally, don't forget to factor in any upcoming expenses or investments. Are there any big projects on the horizon that will require additional funding? By planning ahead and budgeting for these expenses, you can avoid any last-minute cashflow crunches.

Problem-Solving Solutions:

Budgeting and Forecasting: As a business owner, creating a detailed budget and forecasting future cashflows becomes paramount. Analyze historical data to anticipate fluctuations in income and expenses. Incorporate realistic projections considering the current economic conditions. Regularly revisit and adjust your budget and forecasts as needed.

Cash Reserve Management: Establishing and maintaining a healthy cash reserve is crucial for business resilience during tough times. Aim to have enough cash on hand to cover essential expenses for several months, including payroll, rent, and utilities. Prioritize building up this reserve to withstand economic downturns and unexpected emergencies.

Strategic Cost-Cutting: Take a close look at your business expenses and identify areas where you can trim costs without sacrificing essential operations. This may involve renegotiating contracts with suppliers, finding more cost-effective solutions for utilities or services, or streamlining inefficient processes. Every dollar saved contributes to preserving your cashflow.

Diversification and Adaptation: Explore opportunities to diversify your revenue streams and adapt your business model to align with changing market dynamics. Consider expanding into new markets, offering complementary products or services, or leveraging technology to reach a wider audience. Being adaptable and open to change can help mitigate the impact of economic uncertainties.

Debt Management: If your business carries debt, focus on managing it strategically to avoid cashflow strain. Explore options such as refinancing at lower interest rates, negotiating extended payment terms with creditors, or consolidating debt to reduce monthly payments. Prioritize paying down high-interest debt to free up cashflow for other business needs.

Customer Relationship Management: Strengthening customer relationships is essential for maintaining steady cashflow. Focus on providing exceptional value and service to retain existing customers and attract new ones. Implement loyalty programs, offer discounts or incentives, and actively seek feedback to ensure customer satisfaction and loyalty.

Investment in Growth Initiatives: While cost-cutting is important during challenging times, don't overlook strategic investments that can fuel long-term growth. Evaluate opportunities to invest in marketing, research and development, staff training, or infrastructure improvements that can enhance your competitive advantage and drive future profitability.

Monitor and Adjust: Keep a close eye on your cashflow metrics and key performance indicators (KPIs) regularly. Set up alerts or reminders to flag any significant deviations from your projections. Be proactive in addressing cashflow challenges by adjusting your strategies and tactics as needed to stay on track toward your business goals.

Finally, I want to encourage you to stay positive. Managing your cashflow can be tough, especially during challenging economic times, but remember that every little step you take towards financial stability is a step in the right direction. You've got this!

So there you have it – a beginner's guide to managing your cashflow for free using spreadsheets. I hope you found this article helpful, and remember, if you ever need a helping hand, don't hesitate to reach out. You've got the power to take control of your finances – go out there and make it happen!

The Power of Accounting Software and Handwritten Ledgers: Tools for "Future-Proof" Tax Success

In finance, particularly for small businesses and freelancers, tax season can oftentimes seem more overwhelming than the task actually could be. However, with your simple record-keeping “old-school style” and the merger of accounting software, navigating through tax obligations has become significantly more manageable. Businesses need efficient and dependable tools to guide the complexities of finance and taxation.

Tax season doesn't have to be synonymous with chaos and confusion. By using the right tools and resources even from your phone, individuals and businesses can streamline their financial processes, gain deeper insights into their financial health, and ultimately achieve greater peace of mind. Preparation is key when it comes to tax season, stay organized throughout the year, making tax filing a seamless process rather than a frantic scramble as the deadline approaches. Making the change to being organized and prepared can start any time of year.

How businesses can benefit from using streamlined accounting software:

Keeping a Ledger: Always keep a list of what money is coming in, from where, the obligations of where it must go (taxes included), what is left over, and where that also should go.

Automation of Financial Tasks: Accounting software automates redundant tasks like invoicing, bills & expense tracking, and banking. Saving time and can reduce the risk of errors, allowing business owners to focus on core activities. As much as we believe online tools are error-proof they are not. Be sure to manually review automations regularly. Take note of any expenses that may have risen. Even pay attention to if any of your service providers have changed their pricing. You are ultimately the main and most capable of accounting for where your money goes.

Real-Time Financial Insights: With accounting software, you have access to real-time financial data and reports. This visibility enables you with informed decision-making, as you track cash flow, monitor expenses, and assess profitability at any given time.

Enhanced Accuracy and Compliance: Accounting software helps ensure accuracy and compliance with tax regulations. It automates tax calculations, generates compliant financial statements, and facilitates easy tax filing, reducing the risk of errors and penalties.

Improved Cash Flow Management: By tracking income and expenses in real-time, accounting software enables better cash flow management and accountability. Business owners can identify trends, anticipate financial needs, and make proactive adjustments to optimize cash flow.

Facilitated Business Growth: Streamlined accounting processes facilitate business growth by providing scalable solutions. As businesses expand, accounting software can accommodate increased transactions, users, and reporting requirements without compromising efficiency.

Integration with Other Systems: Accounting software often integrates seamlessly with other business systems, such as payroll, inventory management, banking and CRM software. This integration streamlines workflows, eliminates data silos, and enhances overall operational efficiency.

Accessibility and Mobility: Cloud-based accounting software offers anytime, anywhere access to financial data via the Internet, your phone included. This accessibility allows business owners to manage finances on the go, collaborate with team members remotely, and respond promptly to business needs.

QuickBooks stands out as a game-changer in financial management software. It offers a user-friendly interface, powerful features, and full-bodied functionality tailored to the needs of small businesses and self-employed individuals.

Strength of Handwritten Ledgers Alongside Digital Tools

At a time when technology reigns supreme, the thought of using a pen and paper to record financial transactions might seem out-of-date. However, blending handwritten ledgers with digital tools offers a diligent approach to financial management and ensures no “sneak leaking” of funds. Do not limit the advantages of this hybrid method and it's worth implementing for anyone in personal and business finances.

The Internal & Emotional Sensory Experience:

There's a certain fulfillment that comes with the act of writing by hand. Unlike typing on a keyboard, physically recording transactions engages multiple senses, enhancing understanding and retention of information. For entrepreneurs seeking a deeper connection with their finances, the process of manually jotting down transactions in a ledger can provide valuable insights into cash flow, expenses, and overall financial health. Oh, and writing has this effect in general!

Enhanced Security and Backup:

While digital tools offer convenience, they also come with the risk of technological glitches or security breaches. By maintaining a handwritten ledger alongside digital records, entrepreneurs create a reliable backup system. In the event of a digital failure or loss, having a physical record ensures the continuity of financial data and provides peace of mind. It's an extra layer of security in an increasingly digital world.

Synergy of Analog and Digital:

The combination of handwritten ledgers and digital tools offers the best of both worlds. Online platforms provide automation, real-time insights, and seamless integration, while handwritten records offer a personal touch and serve as a backup. By welcoming this hybrid process, entrepreneurs can enjoy the benefits of modern technology while retaining the authenticity of handwritten records.

Promoting Financial Literacy:

Understanding the intricacies of financial management is essential for entrepreneurs. By actively engaging with financial data through handwritten ledgers, individuals can deepen their financial literacy and make more informed decisions about their businesses. It's a hands-on approach that fosters a deeper connection with one's finances and promotes a greater sense of control and understanding.

Why QuickBooks is a Game-Changer for Tax Season

QuickBooks streamlines tax season by automating monotonous tasks, delivering real-time understandings of financial data, and offering extended reporting abilities. Its instinctive design and accessibility make it an integral tool for businesses of all sizes. QuickBooks is a top accounting software that provides users with tools for invoicing, expense tracking, payroll management, and more. Its user-friendly interface and customizable features make it an ideal solution for businesses of all sizes.

Tool #1: QuickBooks Online

Features that Make a Difference

QuickBooks Online boasts an array of features designed to facilitate financial management and tax preparation. From automated expense tracking to seamless invoice management, it simplifies the entire process from start to finish.

Automated Expense Tracking: QuickBooks Online automatically categorizes expenses and syncs with bank accounts, saving time and reducing manual entry errors.

Invoice Management: Users can create professional invoices, track payments, and send automatic reminders, improving cash flow management.

Step-by-Step Guide to Maximizing QuickBooks Online

Opening the full potential of QuickBooks Online is easier than you might think. By following a few simple steps, users can harness its features to optimize their tax preparation efforts and drive business success.

To maximize the benefits of QuickBooks Online during tax season, businesses should:

Set up bank account syncing for seamless expense tracking.

Customize invoice templates to reflect branding and ensure professionalism.

Utilize reporting tools to gain insights into financial performance and tax liabilities.

Tool #2: QuickBooks Self-Employed

Tailored for the Freelancer and Solopreneur

QuickBooks Self-Employed caters particularly to the unique needs of freelancers and solopreneurs. Its characteristics, such as mileage tracking and simplified tax deductions, empower individuals to take control of their finances with ease.

QuickBooks Self-Employed caters to the unique needs of freelancers, providing features such as:

Mileage Tracking: Users can track mileage automatically using the mobile app, ensuring accurate deductions for business-related travel.

Tax Deductions Simplified: QuickBooks Self-Employed categorizes expenses and identifies potential deductions, helping users save money during tax season.

Navigating QuickBooks Self-Employed for Tax Advantages

With QuickBooks Self-Employed, tax preparation becomes a breeze. By accurately tracking expenses, maximizing deductions, and staying organized year-round, freelancers can minimize our tax liability and maximize our financial well-being.

To leverage QuickBooks Self-Employed effectively for tax advantages, freelancers should:

Use the mobile app to track mileage for business-related travel.

Categorize expenses accurately to maximize deductions.

Utilize the tax preparation feature to estimate quarterly taxes and avoid surprises at year-end.

Tool #3: QuickBooks Payroll

Ensuring Employee Satisfaction and Tax Compliance

For businesses with employees, QuickBooks Payroll offers invaluable assistance in managing payroll taxes and ensuring compliance with tax regulations. Its automated features streamline the payroll process, saving time and reducing the risk of errors.

QuickBooks Payroll offers features such as:

Automated Payroll Taxes: The software calculates and withholds payroll taxes automatically, reducing the risk of errors and penalties.

Employee Payment Features: Users can pay employees via direct deposit or printed checks, streamlining the payroll process and improving employee satisfaction.

Leveraging QuickBooks Payroll for Smooth Tax Seasons

By integrating QuickBooks Payroll into their operations, businesses can mitigate the stress associated with tax season. With features like automated tax calculations and employee payment capabilities, they can focus on running their business with confidence.

To leverage QuickBooks Payroll effectively during tax season, businesses should:

Ensure accurate employee data and tax withholdings to avoid discrepancies.

Use the reporting feature to generate payroll reports for tax filing purposes.

Stay updated on tax regulations and deadlines to ensure compliance.

Integrating QuickBooks Tools into Your Business

Tips for Seamless Integration

Successfully incorporating QuickBooks tools into your business requires careful planning and execution. By following best practices and seeking aid when needed, businesses can maximize the benefits of these powerful software solutions.

Customize Settings: Tailor QuickBooks settings to align with business preferences and workflows.

Training and Support: Provide employees with training and support to ensure proper utilization of QuickBooks tools.

Regular Updates: Stay informed about new features and updates to take full advantage of QuickBooks' capabilities.

Future-Proofing Your Business

Adding a Personal Touch:

In an increasingly automated world, the personal touch of handwritten records adds a sense of authenticity to financial management. It's a reminder of the human aspect behind every transaction and serves as a reflection of individuality and creativity. For entrepreneurs who value authenticity and personal connection, maintaining a handwritten ledger is a meaningful way to infuse personality into their financial processes.

Blending handwritten ledgers with digital tools offers a powerful approach to financial management for modern entrepreneurs. By harnessing the strengths of both analog and digital methods, individuals can enjoy the sensory satisfaction of pen and paper while leveraging the efficiency and convenience of technology. So, whether you're a small business owner or a solopreneur, consider embracing this hybrid approach to unlock new insights and streamline your financial processes.

Staying Ahead of Tax Legislation Changes

Tax laws and regulations are constantly evolving. Businesses should stay informed about changes in tax laws, regulations, and filing requirements at the local, state, and federal levels. This includes keeping abreast of updates from tax authorities, legislative bodies, and professional associations. Review and update tax policies, procedures, and internal controls regularly to align with changes in tax laws and regulations. This ensures that businesses remain compliant and minimize the risk of non-compliance penalties or audits.

Consult with Tax Professionals

Working with tax professionals, such as accountants or tax advisors, can provide valuable insights into regulatory changes and their implications for businesses. Tax professionals can offer personalized guidance, help interpret complex tax laws, and recommend appropriate strategies for compliance and tax optimization. Establishing open communication channels with tax advisors and legal experts fosters collaboration and enables businesses to address tax-related concerns promptly. Regular consultations with advisors can help businesses navigate complex tax issues and adapt to legislative changes effectively.

Continuous Learning and Adaptation

Proactive tax planning can help businesses minimize tax liabilities and maximize tax savings opportunities within the bounds of the law. By leveraging tax planning strategies such as deductions, credits, and incentives, businesses can optimize their tax position and preserve financial resources. By staying informed about new features and best practices, businesses can future-proof their operations and maintain their competitive edge.

With the evolution of sophisticated accounting software, navigating through tax obligations has become more manageable than ever before. By leveraging streamlined solutions, individuals and businesses can transform tax season into an opportunity for greater financial empowerment and success.

While online tools offer automation, real-time insights, and seamless integration, incorporating a handwritten ledger alongside these digital resources can provide additional benefits. The tactile experience of physically recording transactions can enhance understanding and retention of financial data. Additionally, a handwritten ledger serves as a backup in case of technological failures or data breaches, ensuring the continuity of financial records.

Preparation is paramount. Whether utilizing online tools, a handwritten ledger, or a combination of both, staying organized throughout the year and remaining vigilant about tax legislation changes are essential. By doing so, entrepreneurs can future-proof their businesses, minimize tax liabilities, and achieve their financial goals. With the right tools and strategies, you're equipped to conquer tax season and stride toward greater success.

FAQ:

1. How can accounting software streamline tax preparation?

Modern accounting software simplifies tax preparation by automating tasks, providing real-time insights, and offering comprehensive reporting capabilities. By tracking expenses, managing deductions, and ensuring compliance, entrepreneurs can navigate tax season with ease and accuracy.

2. Why should entrepreneurs consider using both online tools and handwritten ledgers for financial management?

Combining online tools with handwritten ledgers offers a comprehensive approach to financial management. While online tools provide automation and real-time insights, handwritten ledgers offer tactile engagement and serve as a reliable backup in case of technological failures.

3. How can a handwritten ledger complement online accounting software during tax preparation?

A handwritten ledger enhances understanding and retention of financial data while serving as a backup in case of technological failures. By incorporating both methods, entrepreneurs can ensure the continuity of financial records and minimize the risk of data loss.

4. What are the benefits of maintaining a handwritten ledger alongside online tools?

In addition to providing a backup for digital records, a handwritten ledger offers tactile engagement and can enhance comprehension of financial data. This dual approach combines the convenience of online tools with the reliability of handwritten records.

5. How can entrepreneurs effectively integrate a handwritten ledger into their financial management processes?

Integrating a handwritten ledger into financial management processes requires careful coordination with online tools. Entrepreneurs can designate specific transactions for manual entry in the ledger while utilizing online tools for automation and real-time insights. This hybrid approach maximizes the benefits of both methods and ensures comprehensive financial management.