"Stop Mixing Business and Personal Travel Expenses! Discover How Navan Can Save You Time and Money"

Managing business and personal travel expenses can be a complex and often confusing task, especially when both types of expenses occur simultaneously. Not to mention how fast a trip can go by, what receipts weren’t collected, which were, which part was business, and which part was personal.

This article will explore the importance of differentiating and tracking these expenses in an automated way, discuss effective methods for doing so, and highlight how tools like Navan and Refresh.me simplify the process. By the end of this article, you'll have a clear understanding of how to manage your travel expenses efficiently, ensuring compliance with tax regulations and maximizing your travel benefits.

Importance of Tracking Business vs. Personal Expenses

Keeping business and personal expenses separate is crucial for several reasons. Mixing these expenses can lead to accounting errors, making it difficult to accurately report business expenses on your taxes. This can result in lost deductions and potential issues with tax authorities. Additionally, separating expenses ensures better financial management and clarity in understanding your business's profitability.

Real-World Scenario

Imagine you're a small business owner attending a conference in New York. You decide to extend your stay for a personal vacation. Without a clear system in place, it becomes challenging to differentiate the costs associated with the conference (business expense) from your vacation (personal expense). This confusion can lead to incorrect bookkeeping, resulting in either over-reporting or under-reporting your business expenses. How about the tax deductions you could be missing out on?

Methods for Keeping Track of Expenses

Separate Bank Accounts and Credit Cards: Use dedicated accounts and cards for business transactions. This helps in easily identifying and tracking expenses without the need to sift through mixed transactions.

Detailed Expense Reports: Maintain detailed records of your expenses. Include receipts, dates, descriptions, and the purpose of each expense. This practice helps in accurately categorizing expenses and supports your claims during tax filing.

Digital Tools and Apps: Utilize expense tracking software like Navan and Refresh.me. These tools automate the tracking process, ensuring accuracy and saving time.

How Navan Simplifies Expense Tracking

Navan offers a comprehensive solution for managing travel expenses. Here’s how:

Automatic Categorization: Navan automatically categorizes expenses as business or personal based on predefined rules. This feature reduces manual effort and minimizes errors.

Integration: By automating the reconciliation process and integrating directly with tools like Refresh.me and QuickBooks Online, finance teams can eliminate frustrating, manual work and close the books faster.

Real-Time Expense Tracking: With real-time tracking, you can monitor your expenses as they occur, ensuring immediate identification and correction of any discrepancies.

Integration with Accounting Software: Navan integrates seamlessly with popular accounting tools, ensuring that your expense data is always up-to-date and accurate.

How Refresh.me Enhances Expense Management

Refresh.me complements Navan by providing additional features for expense management:

Expense Insights and Analytics: Refresh.me offers detailed insights and analytics, helping you understand spending patterns and make informed decisions.

Customizable Reports: Generate customized reports that meet your specific needs, whether for tax filing or internal reviews.

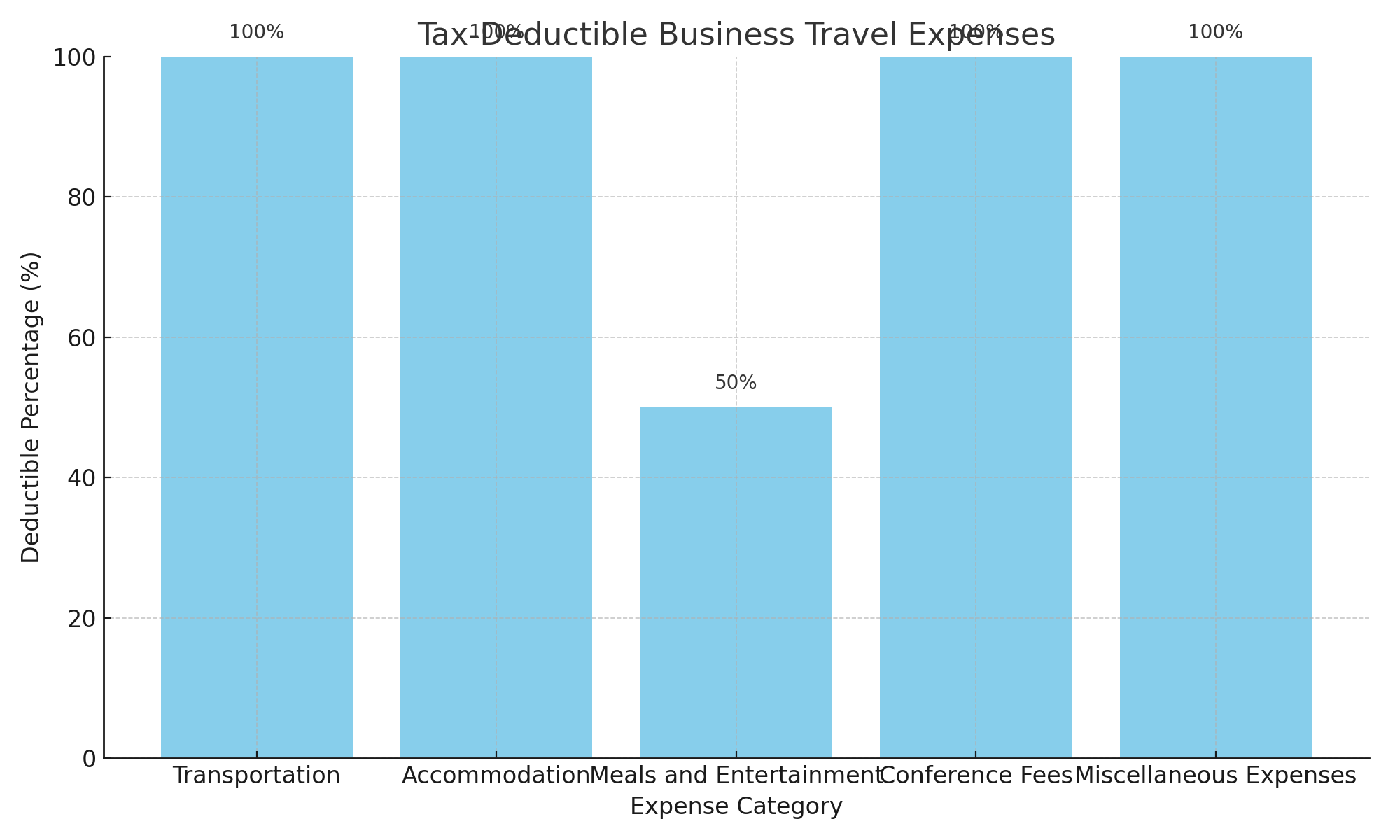

What Business Travel Expenses are Tax-Deductible

Understanding what qualifies as a tax-deductible business travel expense is crucial. Common deductible expenses include:

Transportation: Costs of flights, trains, taxis, and car rentals for business purposes.

Accommodation: Hotel stays and lodging expenses incurred during business trips.

Meals and Entertainment: Business-related meals and entertainment, typically up to 50% of the cost.

Conference Fees: Registration fees for business-related conferences and events.

Miscellaneous Expenses: Other necessary expenses such as internet fees, shipping of business materials, and tips.

Business Tax Deductible Expenses

Effectively managing business and personal travel expenses is essential for maintaining accurate financial records and maximizing tax benefits. By using tools like Navan and Refresh.me, you can simplify the tracking process, ensure compliance with tax regulations, and gain valuable insights into your spending patterns. Start integrating these solutions into your financial management practices today to experience the benefits firsthand.

For further reading on expense management and financial tools, check out our other articles and resources. Don't forget to subscribe to our newsletter for the latest tips and updates!

The Power of Accounting Software and Handwritten Ledgers: Tools for "Future-Proof" Tax Success

In finance, particularly for small businesses and freelancers, tax season can oftentimes seem more overwhelming than the task actually could be. However, with your simple record-keeping “old-school style” and the merger of accounting software, navigating through tax obligations has become significantly more manageable. Businesses need efficient and dependable tools to guide the complexities of finance and taxation.

Tax season doesn't have to be synonymous with chaos and confusion. By using the right tools and resources even from your phone, individuals and businesses can streamline their financial processes, gain deeper insights into their financial health, and ultimately achieve greater peace of mind. Preparation is key when it comes to tax season, stay organized throughout the year, making tax filing a seamless process rather than a frantic scramble as the deadline approaches. Making the change to being organized and prepared can start any time of year.

How businesses can benefit from using streamlined accounting software:

Keeping a Ledger: Always keep a list of what money is coming in, from where, the obligations of where it must go (taxes included), what is left over, and where that also should go.

Automation of Financial Tasks: Accounting software automates redundant tasks like invoicing, bills & expense tracking, and banking. Saving time and can reduce the risk of errors, allowing business owners to focus on core activities. As much as we believe online tools are error-proof they are not. Be sure to manually review automations regularly. Take note of any expenses that may have risen. Even pay attention to if any of your service providers have changed their pricing. You are ultimately the main and most capable of accounting for where your money goes.

Real-Time Financial Insights: With accounting software, you have access to real-time financial data and reports. This visibility enables you with informed decision-making, as you track cash flow, monitor expenses, and assess profitability at any given time.

Enhanced Accuracy and Compliance: Accounting software helps ensure accuracy and compliance with tax regulations. It automates tax calculations, generates compliant financial statements, and facilitates easy tax filing, reducing the risk of errors and penalties.

Improved Cash Flow Management: By tracking income and expenses in real-time, accounting software enables better cash flow management and accountability. Business owners can identify trends, anticipate financial needs, and make proactive adjustments to optimize cash flow.

Facilitated Business Growth: Streamlined accounting processes facilitate business growth by providing scalable solutions. As businesses expand, accounting software can accommodate increased transactions, users, and reporting requirements without compromising efficiency.

Integration with Other Systems: Accounting software often integrates seamlessly with other business systems, such as payroll, inventory management, banking and CRM software. This integration streamlines workflows, eliminates data silos, and enhances overall operational efficiency.

Accessibility and Mobility: Cloud-based accounting software offers anytime, anywhere access to financial data via the Internet, your phone included. This accessibility allows business owners to manage finances on the go, collaborate with team members remotely, and respond promptly to business needs.

QuickBooks stands out as a game-changer in financial management software. It offers a user-friendly interface, powerful features, and full-bodied functionality tailored to the needs of small businesses and self-employed individuals.

Strength of Handwritten Ledgers Alongside Digital Tools

At a time when technology reigns supreme, the thought of using a pen and paper to record financial transactions might seem out-of-date. However, blending handwritten ledgers with digital tools offers a diligent approach to financial management and ensures no “sneak leaking” of funds. Do not limit the advantages of this hybrid method and it's worth implementing for anyone in personal and business finances.

The Internal & Emotional Sensory Experience:

There's a certain fulfillment that comes with the act of writing by hand. Unlike typing on a keyboard, physically recording transactions engages multiple senses, enhancing understanding and retention of information. For entrepreneurs seeking a deeper connection with their finances, the process of manually jotting down transactions in a ledger can provide valuable insights into cash flow, expenses, and overall financial health. Oh, and writing has this effect in general!

Enhanced Security and Backup:

While digital tools offer convenience, they also come with the risk of technological glitches or security breaches. By maintaining a handwritten ledger alongside digital records, entrepreneurs create a reliable backup system. In the event of a digital failure or loss, having a physical record ensures the continuity of financial data and provides peace of mind. It's an extra layer of security in an increasingly digital world.

Synergy of Analog and Digital:

The combination of handwritten ledgers and digital tools offers the best of both worlds. Online platforms provide automation, real-time insights, and seamless integration, while handwritten records offer a personal touch and serve as a backup. By welcoming this hybrid process, entrepreneurs can enjoy the benefits of modern technology while retaining the authenticity of handwritten records.

Promoting Financial Literacy:

Understanding the intricacies of financial management is essential for entrepreneurs. By actively engaging with financial data through handwritten ledgers, individuals can deepen their financial literacy and make more informed decisions about their businesses. It's a hands-on approach that fosters a deeper connection with one's finances and promotes a greater sense of control and understanding.

Why QuickBooks is a Game-Changer for Tax Season

QuickBooks streamlines tax season by automating monotonous tasks, delivering real-time understandings of financial data, and offering extended reporting abilities. Its instinctive design and accessibility make it an integral tool for businesses of all sizes. QuickBooks is a top accounting software that provides users with tools for invoicing, expense tracking, payroll management, and more. Its user-friendly interface and customizable features make it an ideal solution for businesses of all sizes.

Tool #1: QuickBooks Online

Features that Make a Difference

QuickBooks Online boasts an array of features designed to facilitate financial management and tax preparation. From automated expense tracking to seamless invoice management, it simplifies the entire process from start to finish.

Automated Expense Tracking: QuickBooks Online automatically categorizes expenses and syncs with bank accounts, saving time and reducing manual entry errors.

Invoice Management: Users can create professional invoices, track payments, and send automatic reminders, improving cash flow management.

Step-by-Step Guide to Maximizing QuickBooks Online

Opening the full potential of QuickBooks Online is easier than you might think. By following a few simple steps, users can harness its features to optimize their tax preparation efforts and drive business success.

To maximize the benefits of QuickBooks Online during tax season, businesses should:

Set up bank account syncing for seamless expense tracking.

Customize invoice templates to reflect branding and ensure professionalism.

Utilize reporting tools to gain insights into financial performance and tax liabilities.

Tool #2: QuickBooks Self-Employed

Tailored for the Freelancer and Solopreneur

QuickBooks Self-Employed caters particularly to the unique needs of freelancers and solopreneurs. Its characteristics, such as mileage tracking and simplified tax deductions, empower individuals to take control of their finances with ease.

QuickBooks Self-Employed caters to the unique needs of freelancers, providing features such as:

Mileage Tracking: Users can track mileage automatically using the mobile app, ensuring accurate deductions for business-related travel.

Tax Deductions Simplified: QuickBooks Self-Employed categorizes expenses and identifies potential deductions, helping users save money during tax season.

Navigating QuickBooks Self-Employed for Tax Advantages

With QuickBooks Self-Employed, tax preparation becomes a breeze. By accurately tracking expenses, maximizing deductions, and staying organized year-round, freelancers can minimize our tax liability and maximize our financial well-being.

To leverage QuickBooks Self-Employed effectively for tax advantages, freelancers should:

Use the mobile app to track mileage for business-related travel.

Categorize expenses accurately to maximize deductions.

Utilize the tax preparation feature to estimate quarterly taxes and avoid surprises at year-end.

Tool #3: QuickBooks Payroll

Ensuring Employee Satisfaction and Tax Compliance

For businesses with employees, QuickBooks Payroll offers invaluable assistance in managing payroll taxes and ensuring compliance with tax regulations. Its automated features streamline the payroll process, saving time and reducing the risk of errors.

QuickBooks Payroll offers features such as:

Automated Payroll Taxes: The software calculates and withholds payroll taxes automatically, reducing the risk of errors and penalties.

Employee Payment Features: Users can pay employees via direct deposit or printed checks, streamlining the payroll process and improving employee satisfaction.

Leveraging QuickBooks Payroll for Smooth Tax Seasons

By integrating QuickBooks Payroll into their operations, businesses can mitigate the stress associated with tax season. With features like automated tax calculations and employee payment capabilities, they can focus on running their business with confidence.

To leverage QuickBooks Payroll effectively during tax season, businesses should:

Ensure accurate employee data and tax withholdings to avoid discrepancies.

Use the reporting feature to generate payroll reports for tax filing purposes.

Stay updated on tax regulations and deadlines to ensure compliance.

Integrating QuickBooks Tools into Your Business

Tips for Seamless Integration

Successfully incorporating QuickBooks tools into your business requires careful planning and execution. By following best practices and seeking aid when needed, businesses can maximize the benefits of these powerful software solutions.

Customize Settings: Tailor QuickBooks settings to align with business preferences and workflows.

Training and Support: Provide employees with training and support to ensure proper utilization of QuickBooks tools.

Regular Updates: Stay informed about new features and updates to take full advantage of QuickBooks' capabilities.

Future-Proofing Your Business

Adding a Personal Touch:

In an increasingly automated world, the personal touch of handwritten records adds a sense of authenticity to financial management. It's a reminder of the human aspect behind every transaction and serves as a reflection of individuality and creativity. For entrepreneurs who value authenticity and personal connection, maintaining a handwritten ledger is a meaningful way to infuse personality into their financial processes.

Blending handwritten ledgers with digital tools offers a powerful approach to financial management for modern entrepreneurs. By harnessing the strengths of both analog and digital methods, individuals can enjoy the sensory satisfaction of pen and paper while leveraging the efficiency and convenience of technology. So, whether you're a small business owner or a solopreneur, consider embracing this hybrid approach to unlock new insights and streamline your financial processes.

Staying Ahead of Tax Legislation Changes

Tax laws and regulations are constantly evolving. Businesses should stay informed about changes in tax laws, regulations, and filing requirements at the local, state, and federal levels. This includes keeping abreast of updates from tax authorities, legislative bodies, and professional associations. Review and update tax policies, procedures, and internal controls regularly to align with changes in tax laws and regulations. This ensures that businesses remain compliant and minimize the risk of non-compliance penalties or audits.

Consult with Tax Professionals

Working with tax professionals, such as accountants or tax advisors, can provide valuable insights into regulatory changes and their implications for businesses. Tax professionals can offer personalized guidance, help interpret complex tax laws, and recommend appropriate strategies for compliance and tax optimization. Establishing open communication channels with tax advisors and legal experts fosters collaboration and enables businesses to address tax-related concerns promptly. Regular consultations with advisors can help businesses navigate complex tax issues and adapt to legislative changes effectively.

Continuous Learning and Adaptation

Proactive tax planning can help businesses minimize tax liabilities and maximize tax savings opportunities within the bounds of the law. By leveraging tax planning strategies such as deductions, credits, and incentives, businesses can optimize their tax position and preserve financial resources. By staying informed about new features and best practices, businesses can future-proof their operations and maintain their competitive edge.

With the evolution of sophisticated accounting software, navigating through tax obligations has become more manageable than ever before. By leveraging streamlined solutions, individuals and businesses can transform tax season into an opportunity for greater financial empowerment and success.

While online tools offer automation, real-time insights, and seamless integration, incorporating a handwritten ledger alongside these digital resources can provide additional benefits. The tactile experience of physically recording transactions can enhance understanding and retention of financial data. Additionally, a handwritten ledger serves as a backup in case of technological failures or data breaches, ensuring the continuity of financial records.

Preparation is paramount. Whether utilizing online tools, a handwritten ledger, or a combination of both, staying organized throughout the year and remaining vigilant about tax legislation changes are essential. By doing so, entrepreneurs can future-proof their businesses, minimize tax liabilities, and achieve their financial goals. With the right tools and strategies, you're equipped to conquer tax season and stride toward greater success.

FAQ:

1. How can accounting software streamline tax preparation?

Modern accounting software simplifies tax preparation by automating tasks, providing real-time insights, and offering comprehensive reporting capabilities. By tracking expenses, managing deductions, and ensuring compliance, entrepreneurs can navigate tax season with ease and accuracy.

2. Why should entrepreneurs consider using both online tools and handwritten ledgers for financial management?

Combining online tools with handwritten ledgers offers a comprehensive approach to financial management. While online tools provide automation and real-time insights, handwritten ledgers offer tactile engagement and serve as a reliable backup in case of technological failures.

3. How can a handwritten ledger complement online accounting software during tax preparation?

A handwritten ledger enhances understanding and retention of financial data while serving as a backup in case of technological failures. By incorporating both methods, entrepreneurs can ensure the continuity of financial records and minimize the risk of data loss.

4. What are the benefits of maintaining a handwritten ledger alongside online tools?

In addition to providing a backup for digital records, a handwritten ledger offers tactile engagement and can enhance comprehension of financial data. This dual approach combines the convenience of online tools with the reliability of handwritten records.

5. How can entrepreneurs effectively integrate a handwritten ledger into their financial management processes?

Integrating a handwritten ledger into financial management processes requires careful coordination with online tools. Entrepreneurs can designate specific transactions for manual entry in the ledger while utilizing online tools for automation and real-time insights. This hybrid approach maximizes the benefits of both methods and ensures comprehensive financial management.

How To Handle Taxes For First-Time Homeowners

Tax season can be the most exciting or anxious time of the year for anyone. It can be a little stressful when you're not ready for something. If you have or are moving into a new home, you might wonder what else you should know.

Co-authored by:

Andrew Latham Certified Financial Planner & a Director at SuperMoney.com

Tax season can be the most exciting or anxious time of the year for anyone. It can be a little stressful when you're not ready for something. If you have or are moving into a new home, you might wonder what else you should know.

What you should remember as you prepare for tax season this year:

Who is considered a first-time homebuyer?

Who qualifies as a first-time buyer?

The current reality of First-time Homeowner Taxes & steps to get Ready: Co-Authored by Andrew Latham of SuperMoney.com

What is the First-Time Homebuyer Act of 2021?

What are first-time buyer tax credits?

How does the $15,000 tax credit for first-time homebuyers operate?

Take advantage of available tax deductions.

Conclusion

Who is considered a first-time homebuyer?

It would be best if you met a few conditions to get a first-time homebuyer's tax credit. The credit isn't just for people who may have never bought a home, despite what its name says. If you haven't owned a home or been a cosigner on a mortgage in the last three years, you are considered a first-time homebuyer.

You must meet one of the following requirements to qualify as a first-time buyer:

Have not owned a house or been a cosigner on a home loan in the past three years

Be a single parent who only owned a home with a former spouse when they were married. Be a displaced homemaker who only owned a home with a spouse.

Have only lived in a house that was fixed to a foundation.

Have only owned a home that doesn't meet state or local building codes and can't be fixed for less than what it would cost to build a permanent structure.

The current reality of First-time Homeowner Taxes & Getting Ready: Co-Authored by Andrew Latham of SuperMoney.com

Buying a home for the first time can be an exciting but overwhelming experience. The tax side of things is pretty straightforward, though. As long as you pay your property taxes, you should be fine. Realtors like to wax poetic on the tax benefits of buying a home, but the truth is most homeowners don't get much nowadays.

The Tax Cuts and Jobs Act (TCJA) reduced the maximum mortgage principal eligible for the tax deduction, removed the personal exemption, and nearly doubled standard deductions. These changes made it pointless for most taxpayers to itemize since they could no longer take both the personal exemption and itemized deductions. In most cases, first-time homebuyers are better off claiming the standard deduction even if they do qualify to itemize the mortgage interest payments.

That doesn't mean buying a house doesn't come with extra tax homework. The first step is to get organized. As soon as you close on your home, gather all of the documents related to your purchase and keep them in a safe place. This includes your mortgage statement, closing statement, property tax bill, and any other related documents.

As a first-time homeowner, you may be eligible for certain tax benefits, such as the mortgage interest deduction and the property tax deduction. However, these deductions don't apply to most homeowners because the vast majority of homeowners are better off claiming the standard deduction. Nevertheless, itemizing does make sense for some homeowners, so do the math and check which option works best for you.

Keep track of home improvements. If you make any improvements to your home, make sure to keep track of the costs. These improvements can also be tax-deductible, so it's important to have documentation of the costs.

Keep accurate records. Make sure to keep accurate records of all your expenses related to your home. This will make it easier to claim deductions and credits on your taxes.

Hire a tax professional. If you're unsure about how to handle your taxes as a first-time homeowner, consider hiring a tax professional to help you navigate the process. Most tax preparation programs, such as TurboTax and TaxAct, are all you need to navigate homeowner tax questions, but in some cases hiring a tax professional can save you a lot of time and money. They can answer any questions you have and ensure that you're taking advantage of all the tax benefits available to you.

What is the First-Time Homebuyer Act of 2021?

Several Democratic lawmakers put forward the First-Time Homebuyer Act of 2021 in response to a campaign promise made by President Joe Biden. This bill would have brought the tax credit first used after the housing crisis in 2008. It would have included many of the same requirements.

Under the new bill, however, eligible homebuyers could get a tax credit of up to 10% of the purchase price of their home, up to a maximum of $15,000. The proposed homeowner tax credit for 2021 is meant to help low-income and middle-income Americans buy homes and build wealth in communities of color that will last for generations. This bill hasn't been signed into law as of December 2022.

What are first-time buyer tax credits?

Tax credits are a method by which the government rewards taxpayers financially for doing certain things or acting in certain ways. When you file their tax return, they directly lower the amount of tax you owe. For instance, if you owed $10,000 in federal taxes and got a $1,000 tax credit, your tax bill would drop to $9,000.

Tax credits are a better way to get people to do something than deductions, which let you lower your taxable income. Deductions lower the amount of taxes you have to pay, but not as much as a credit for the exact amount. People who buy their first home can get credits against their federal income taxes through first-time homebuyer tax credits.

How does the $15,000 tax credit for first-time homebuyers operate?

The first-time homebuyer tax credit in 2021 would work the same way as the one in 2008. Homebuyers who were eligible could get a loan for up to 10% of the purchase price of their home, up to a maximum of $15,000.

Unfortunately, this credit no longer exists. However, bills to create a new refundable tax credit of up to $15,000 for first-time homebuyers were introduced in April 2021. As of March 2023, the legislation still has not passed in Congress.

Even though the original first-time homebuyer credit from 2008 has ended and the First-Time Homebuyer Act of 2021 has not yet been officially passed, there are still some other programs you can glance into as a new homeowner:

Mortgage interest deductions:

This detailed deduction lets homeowners take any interest they paid on loan for their home and deduct it from their taxable income. You'll need proof this tax season to get the mortgage interest deduction. The lender you used to buy your home will send you a 1098 Form that shows how much interest you paid on your mortgage over the past year.

Read Also: Google Analytics Tracking Optimization Tips

Property tax reductions:

When you buy your first home, paying property taxes can be scary. However, when it's time to file your taxes, you can write off the state and local property taxes you've paid. You can get a tax break for your main home, vacation home, land, cars, and boats.

Home office costs:

Over the past two years, more people have started working from home. This may have caused your costs for home office supplies to go through the roof. Depending on what you bought, you might be able to get a tax break if you are self-employed or work from home full-time. If you want to save money on your tax return for office costs, your room must be used mostly as an office and be less than 300 square feet.

Conclusion

If the First-Time Homebuyer Act of 2021 becomes law, many Americans with low and middle incomes could get a tax credit for buying a home. Plus, you wouldn't have to pay back the tax credit unless you sold the house in the first four years of owning it.

In the meantime, first-time homebuyers must look into programs like FHA loans, MCCs, and IRA withdrawals that can help them buy a home for less money. If you just bought a home, ensure you understand what costs you can deduct from your taxes. This could help you pay less in taxes.