How to Choose the Best Virtual Business Bank Account?

The way we manage money has evolved rapidly over the past decade. Gone are the days when you had to visit a physical branch for every banking need. Today, many entrepreneurs are turning to virtual business bank accounts to streamline operations, reduce fees, and keep pace with a digital-first world.

But which virtual bank account is right for you—especially if you have $10,000 or more …or less to deposit? What if you are just starting? In this extended companion, we’ll explore the pros and cons of virtual banking, top account options, and what to watch out for as you grow your business.

The Shift from Brick & Mortar to Virtual Business Bank Accounts

A Changing Financial Landscape

Traditional brick-and-mortar banking used to be the gold standard for business owners. You’d walk in, meet a teller, and handle transactions face-to-face. However, the rise of fintech (financial technology) has revolutionized the way businesses manage their finances. Now, you can open an account, transfer funds, and even deposit checks—all without leaving your office.

Advantages of Virtual Banking

Lower Fees: Online banks often have reduced overhead costs, which can translate to fewer or lower fees.

24/7 Accessibility: Manage your account around the clock, from anywhere with internet access.

Streamlined Processes: Automated workflows for invoicing, payroll, and expense management integrate seamlessly with most virtual banks.

Potential Downsides

Limited Physical Access: Depositing large sums of cash or handling urgent matters might be more complicated without a local branch.

Customer Service Challenges: Some online banks rely heavily on email or chat support, which may not be ideal for urgent issues.

Learning Curve: Adopting new platforms and technologies can take time, especially if you’re used to in-person banking.

Key Considerations for Virtual Business Bank Accounts

FDIC Insurance

Make sure the bank you choose is FDIC-insured so your deposits (up to $250,000) are protected. This helps mitigate risk if the bank ever faces financial issues.Fees and Minimum Balance Requirements

Pay close attention to transaction fees, monthly fees, and minimum balance requirements. While many online banks have lower fees than traditional banks, it’s crucial to read the fine print.Access to Cash

If your business deals with physical cash, check for ATM networks or partner institutions that enable hassle-free cash deposits and withdrawals.Technology Integration

The best virtual business bank accounts offer integrations with accounting software (like QuickBooks or Xero), payment processors, and other tools you already use to keep your financials in sync.Customer Support

Look for robust support channels. Some online banks have limited phone support, which might be problematic if you need immediate help.Bank Failure Protocols

With any bank—virtual or traditional—understanding what happens in case of a bank failure can save you stress. Ensure you know about FDIC insurance, backup systems, and how quickly you can access your funds in an emergency.

Best Virtual Business Bank Accounts for Deposits of $10,000 or More

1. Mercury

Why Mercury Stands Out

Heavily Focused on Startups and Tech Companies: Mercury is designed with modern, fast-growing businesses in mind, offering tools that cater specifically to startups.

No Monthly Fees or Minimum Balances: Ideal for businesses that want to avoid hidden costs. Even if you’re depositing more than $10,000, you won’t be penalized if your balance dips occasionally.

Robust Integrations: Mercury integrates seamlessly with platforms like Stripe, QuickBooks, and PayPal, making it easy to manage incoming and outgoing payments.

Virtual Debit Cards: Instantly create virtual cards for online expenses, offering better security and easy tracking.

FDIC Insured via Partner Banks: Mercury partners with multiple institutions, distributing your funds across them to maximize FDIC coverage beyond the standard $250,000 limit if your balances grow.

Potential Drawbacks

No Direct Cash Deposit: Mercury doesn’t support direct cash deposits, which can be an issue if your business regularly handles physical currency.

Limited International Options: While Mercury does support domestic and international wires, the platform is primarily focused on U.S. banking solutions.

Marketing Note: If you’re a growing entrepreneur looking for a sleek, tech-forward solution, Mercury is a go-to choice. They pride themselves on customer-centric design, making it simpler than ever to manage your finances.

2. Bluevine (A Financial Advisor and Attorney’s Perspective)

Why Bluevine Is a Strong Option

High-Interest Checking: Bluevine’s business checking often offers competitive interest rates, enabling you to earn money on your balance.

Easy Online Application: The streamlined application process lets you open an account in just a few minutes—no tedious paperwork required.

FDIC Insured: Through Bluevine’s banking partner, your balance (up to $250,000) is protected.

Broad ATM Network: Bluevine offers fee-free access to a large network of ATMs, which can be a lifesaver if you need cash on the go.

Bill Pay Features: Robust bill payment options let you settle invoices quickly and securely.

Potential Drawbacks

Fees for Certain Transactions: Be mindful of fees for outgoing wires or excess transactions.

Limited Cash Deposit Options: Similar to many online accounts, depositing cash can be more complicated.

Attorney & Advisor Insight: Bluevine’s emphasis on high-yield checking and straightforward digital tools can help you optimize your cash flow. Just keep track of any fees that may chip away at your earnings.

Should You Keep Money in a Local Brick-and-Mortar Bank?

While virtual accounts excel in accessibility and lower fees, having a local bank account can still be beneficial. Physical branches allow you to quickly deposit cash, obtain certified checks, and handle urgent banking matters face-to-face. A balanced approach—where you keep a portion of your funds in an online account and a portion in a local bank—offers the best of both worlds. This way, you’re not locked out of traditional banking services in case of emergencies or widespread technology outages.

What Happens If There Is a Bank Failure?

Financial institutions are heavily regulated, and most reputable online banks ensure your deposits up to $250,000 are FDIC-insured. If the bank fails, the FDIC typically reimburses you promptly for your insured funds. However, any funds above the insured limit could be at risk if the bank collapses. That’s why it’s vital to confirm FDIC coverage and avoid single institutions if you’re managing large balances.

For Businesses with Less Than $10,000: Consider Novo Bank

If your business hasn’t hit the $10,000 mark just yet, Novo Bank is a solid alternative. Novo is designed for freelancers, small business owners, and entrepreneurs who are just starting to grow their revenue.

Why Novo Bank Is a Good Fit

No Hidden Fees: Novo aims for transparency with no monthly fees and free ACH transfers.

Easy-to-Use App: Manage your finances on the go with Novo’s intuitive mobile interface.

Stripe and QuickBooks Integration: Simplify invoicing and accounting without leaving the app.

Multiple Perks: Novo frequently partners with popular services (like Slack, HubSpot, and others) to offer discounts and promos that help you run your business more efficiently.

Potential Downsides

Limited Cash Handling: As with most digital banks, depositing large amounts of physical cash can be a hurdle.

Wire Transfer Fees: Outgoing wire fees may apply, so review the terms carefully.

Key Takeaways:

Choosing the best virtual business bank account largely depends on your deposit size, transaction habits, and tech-savviness. Concerned about safety? Make sure you pick a bank with FDIC insurance and read up on their security measures. Wondering if you should split your funds between multiple banks?

Many entrepreneurs diversify across more than one institution to spread risk and tap into different perks. Worried about cash deposits? A local branch account or a bank with a user-friendly ATM network might be a good backup plan. Wondering how to grow your money while it sits in an account? Look for high-interest checking or savings options, and check for potential fees to ensure your gains aren’t offset by hidden charges.

In the end, virtual banking can be a powerful tool if you choose the right platform. Whether you’re eyeing Mercury for its tech-forward features, Bluevine for its higher interest rates, or Novo for its beginner-friendly approach, do your homework and stay vigilant about security. Combine strong digital options with a traditional backup, and you’ll have the flexibility to weather any financial storms while keeping your business running smoothly.

“Thrive Despite Inflation and Recession: Strategies for an Unstable Economy”

Recent changes in trade policies and ongoing geopolitical tensions shape the economic outlook for the USA in the latter half of 2024. These factors are pivotal in determining the country's economic stability and growth opportunities. Understanding these elements is crucial for business owners to navigate the complex economic landscape effectively.

Trade Policies and Geopolitical Tensions:

Trade Policies: The USA has made some changes in how it trades with other countries. These changes can include tariffs (taxes on imports), trade agreements, and regulations that affect businesses.

Geopolitical Tensions: These are issues like conflicts between countries, political instability, and diplomatic disputes that can impact the global economy.

How These Factors Affect Business Owners

Business owners must grasp how economic stability and growth opportunities are influenced by trade policies and geopolitical tensions. This understanding helps them make informed decisions to safeguard and grow their businesses amidst uncertainty.

Economic Stability: When trade policies change or geopolitical tensions rise, it can lead to economic instability. This means there could be more unpredictability in things like currency exchange rates, supply chain reliability, and market demand.

Growth Opportunities: Shifts in trade policies might open up new markets or close off existing ones. Geopolitical tensions can disrupt global supply chains, making it harder to get materials or sell products abroad.

Navigating the Challenging Economic Times

Given the dual challenges of inflation and recession, navigating the economic landscape requires strategic planning and adaptability. Business owners need to focus on understanding costs, raising prices strategically, and diversifying revenue streams to maintain stability and growth.

1. Inflation and Recession:

Inflation: This is when prices for goods and services rise. It means your money buys less than it did before.

Recession: This is a period when the economy shrinks instead of grows. It can lead to fewer jobs, lower income, and reduced spending by consumers.

Navigating Inflation and Recession:

Understand Costs: Keep a close eye on how much you’re spending on supplies, marketing, and other expenses. Look for ways to reduce these costs without sacrificing quality.

Raise Prices Strategically: If you need to raise prices due to inflation, do it in small increments and communicate clearly with your customers about why the increase is necessary. Let’s be honest, without integrity, this step is a horrible idea. By integrity, we mean, consider the position your customer is also in. Adjust prices back or even better when your industry costs return to normal. Keep great notes since economic waves usually change about every 5 years.

Diversify Revenue Streams: Don’t rely on just one source of income. Look for new products, services, or markets to expand into. Take a fresh look at what you already have to offer.

Managing and Growing Business Finances

Effective financial management is crucial during times of economic instability. Creating a detailed budget, cutting unnecessary costs, and investing in technology can help business owners maintain and grow their finances.

2. Managing and Growing Business Finances:

Budget Wisely: Create a detailed budget that accounts for all your expenses and stick to it. Monitor your finances regularly to ensure you’re staying on track.

Cut Unnecessary Costs: Review your expenses and cut out anything that isn’t essential to your business. Look for more cost-effective alternatives for necessary expenses.

Invest in Technology: Use technology to streamline operations and reduce costs. For example, automation can help reduce labor costs, and software can help manage finances more efficiently.

Lowering Supply, Marketing, and Operational Costs

To maintain profitability, it’s essential to find ways to lower supply, marketing, and operational costs. This involves negotiating with suppliers, utilizing digital marketing, and optimizing operations for efficiency.

3. Lowering Supply, Marketing, and Operational Costs:

Negotiate with Suppliers: Don’t be afraid to negotiate better terms with your suppliers. Long-term relationships can often result in discounts or more favorable payment terms.

Use Digital Marketing: Digital marketing can be more cost-effective than traditional marketing. Use social media, email marketing, and SEO to reach your audience without breaking the bank.

Optimize Operations: Look for inefficiencies in your operations and find ways to streamline them. This could involve automating tasks, outsourcing non-core activities, or improving workflow processes.

Utilizing Existing Resources to Raise Revenue

Maximizing existing resources is a strategic way to increase revenue. Business owners can focus on leveraging data, enhancing customer experience, and maximizing existing customers to boost their income.

4. Utilizing Existing Resources to Raise Revenue:

Maximize Existing Customers: Focus on upselling and cross-selling to your existing customers. It’s often easier and cheaper to sell more to existing customers than to find new ones.

Leverage Data: Use data analytics to understand customer behavior and preferences. This can help you tailor your offerings and marketing strategies to better meet their needs.

Enhance Customer Experience: Providing excellent customer service can lead to repeat business and referrals. Make sure your customers have a positive experience every time they interact with your business.

Juggling Personal Finances Amid Business Changes

Managing personal finances alongside business changes is vital to maintaining overall financial health. Separating business and personal finances, creating an emergency fund, and planning for taxes are key steps to achieve this balance.

5. Juggling Personal Finances Amid Business Changes:

Separate Business and Personal Finances: Keep your business and personal finances separate to avoid confusion and ensure clear tracking of expenses and income.

Create an Emergency Fund: Set aside money in an emergency fund for both personal and business needs. This can help you weather unexpected financial challenges.

Plan for Taxes: Make sure you’re setting aside enough money to cover your tax obligations. Consider working with a tax professional to ensure you’re taking advantage of all available deductions and credits.

In these “shaky ground” times, it’s important to stay informed, adaptable, and proactive. While economic shifts and challenges can seem daunting, there are always ways to navigate and even thrive. Focus on understanding the landscape, managing your finances wisely, and seeking out opportunities for growth. Remember, the road to success is often narrow and requires careful planning and persistence.

Keep learning, stay resilient, and always look for ways to improve and innovate. By being strategic and resourceful, you can turn challenges into opportunities and continue to grow your business even in the face of economic uncertainty. Iron sharpens iron, and by continually honing your skills and knowledge, you can ensure your business not only survives but prospers.

"Stop Mixing Business and Personal Travel Expenses! Discover How Navan Can Save You Time and Money"

Managing business and personal travel expenses can be a complex and often confusing task, especially when both types of expenses occur simultaneously. Not to mention how fast a trip can go by, what receipts weren’t collected, which were, which part was business, and which part was personal.

This article will explore the importance of differentiating and tracking these expenses in an automated way, discuss effective methods for doing so, and highlight how tools like Navan and Refresh.me simplify the process. By the end of this article, you'll have a clear understanding of how to manage your travel expenses efficiently, ensuring compliance with tax regulations and maximizing your travel benefits.

Importance of Tracking Business vs. Personal Expenses

Keeping business and personal expenses separate is crucial for several reasons. Mixing these expenses can lead to accounting errors, making it difficult to accurately report business expenses on your taxes. This can result in lost deductions and potential issues with tax authorities. Additionally, separating expenses ensures better financial management and clarity in understanding your business's profitability.

Real-World Scenario

Imagine you're a small business owner attending a conference in New York. You decide to extend your stay for a personal vacation. Without a clear system in place, it becomes challenging to differentiate the costs associated with the conference (business expense) from your vacation (personal expense). This confusion can lead to incorrect bookkeeping, resulting in either over-reporting or under-reporting your business expenses. How about the tax deductions you could be missing out on?

Methods for Keeping Track of Expenses

Separate Bank Accounts and Credit Cards: Use dedicated accounts and cards for business transactions. This helps in easily identifying and tracking expenses without the need to sift through mixed transactions.

Detailed Expense Reports: Maintain detailed records of your expenses. Include receipts, dates, descriptions, and the purpose of each expense. This practice helps in accurately categorizing expenses and supports your claims during tax filing.

Digital Tools and Apps: Utilize expense tracking software like Navan and Refresh.me. These tools automate the tracking process, ensuring accuracy and saving time.

How Navan Simplifies Expense Tracking

Navan offers a comprehensive solution for managing travel expenses. Here’s how:

Automatic Categorization: Navan automatically categorizes expenses as business or personal based on predefined rules. This feature reduces manual effort and minimizes errors.

Integration: By automating the reconciliation process and integrating directly with tools like Refresh.me and QuickBooks Online, finance teams can eliminate frustrating, manual work and close the books faster.

Real-Time Expense Tracking: With real-time tracking, you can monitor your expenses as they occur, ensuring immediate identification and correction of any discrepancies.

Integration with Accounting Software: Navan integrates seamlessly with popular accounting tools, ensuring that your expense data is always up-to-date and accurate.

How Refresh.me Enhances Expense Management

Refresh.me complements Navan by providing additional features for expense management:

Expense Insights and Analytics: Refresh.me offers detailed insights and analytics, helping you understand spending patterns and make informed decisions.

Customizable Reports: Generate customized reports that meet your specific needs, whether for tax filing or internal reviews.

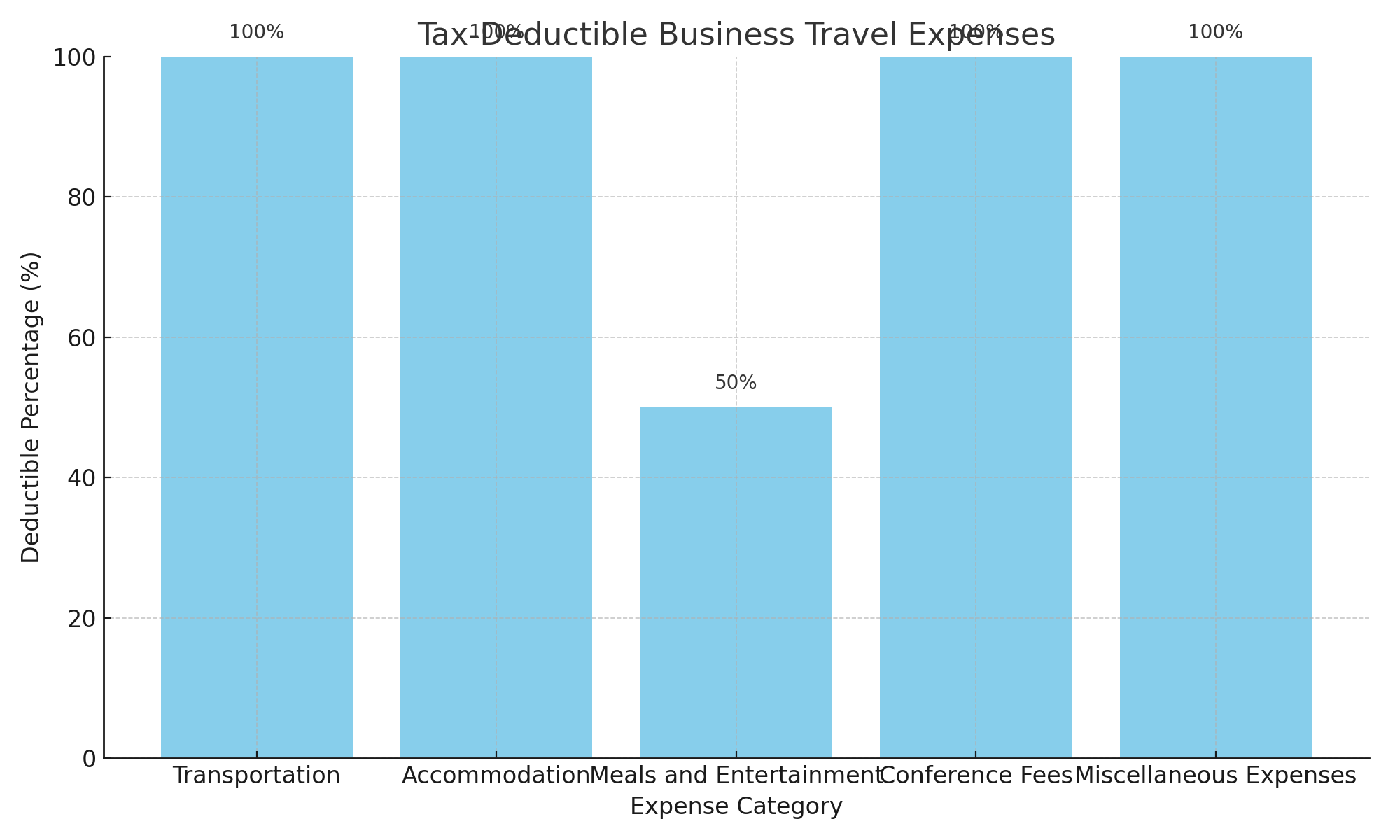

What Business Travel Expenses are Tax-Deductible

Understanding what qualifies as a tax-deductible business travel expense is crucial. Common deductible expenses include:

Transportation: Costs of flights, trains, taxis, and car rentals for business purposes.

Accommodation: Hotel stays and lodging expenses incurred during business trips.

Meals and Entertainment: Business-related meals and entertainment, typically up to 50% of the cost.

Conference Fees: Registration fees for business-related conferences and events.

Miscellaneous Expenses: Other necessary expenses such as internet fees, shipping of business materials, and tips.

Business Tax Deductible Expenses

Effectively managing business and personal travel expenses is essential for maintaining accurate financial records and maximizing tax benefits. By using tools like Navan and Refresh.me, you can simplify the tracking process, ensure compliance with tax regulations, and gain valuable insights into your spending patterns. Start integrating these solutions into your financial management practices today to experience the benefits firsthand.

For further reading on expense management and financial tools, check out our other articles and resources. Don't forget to subscribe to our newsletter for the latest tips and updates!